The Latest Market Trends You Need to Know About Plastic Turnover Boxes

The Latest Market Trends You Need to Know About Plastic Turnover Boxes

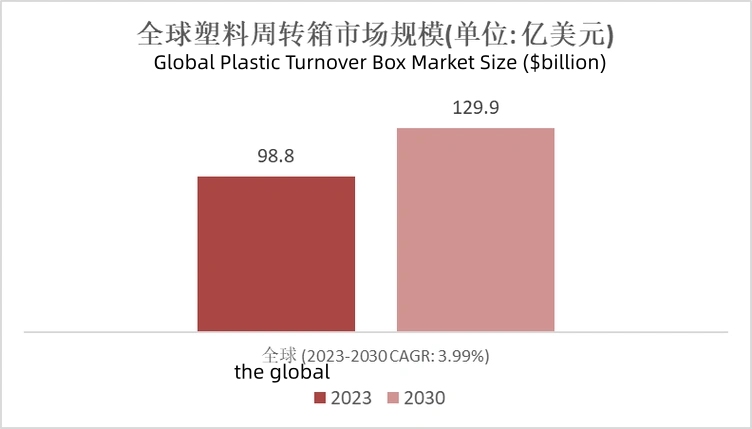

1. Significant Global Market Growth

The global plastic turnover box market is expected to reach $12.68 billion by 2024 and is projected to increase to $15.66 billion by 2031, with a compound annual growth rate (CAGR) of 3.1%.

The growth rate of the Chinese market is leading, with a market size of 22.34 billion yuan, accounting for over 30% of global production capacity, and the demand for logistics and manufacturing industries accounts for over 60%, demonstrating strong development potential.

2. Competitive Strategy: Localization and Customization

International leading enterprises hold dominant advantages through capacity expansion, patented technology, and full lifecycle services. While small and medium-sized manufacturers face homogeneous competition, adapting to the needs of automated warehousing and multimodal transportation through standardized design and scenario customization, to enhance their competitiveness, and meet high demand scenarios such as new energy and cross-border logistics.

3. HDPE/PP Material Technology Advantages

HDPE/PP pure material injection molding has become mainstream, with improved impact resistance. The box meets the hygiene standards of the food and pharmaceutical industry. At the same time, it supports RFID chip embedding, achieving full chain traceability and improving logistics efficiency.

4. Green Cycle and Policy Driven

Recyclable design has become an industry trend. Each company strives to achieve 100% recycling and reduce overall costs.

The 14th Five Year Plan for the Development of Circular Economy in China requires that the utilization rate of recyclable packaging should exceed 50% by 2025, and introduces tax reduction policies to promote the industry's green transformation; The EU PPWR regulation sets limits on packaging carbon emissions, promoting companies to choose environmentally certified products and leading sustainable development.

5. New Developments in Regional Dynamics

North America and Europe are important production areas, but China's growth rate is leading. The Yangtze River Delta and Pearl River Delta regions contribute more than 60% of China's market share. The demand for new energy and automotive parts industries has surged, and it is expected that the global market share will further increase by 2031.

Online message

PowerKing was established in Qingdao in 1997, started with plastic products wholesale business. With 20 years’ continuous efforts and devotion in developing designing and ...

-

PRODUCT

- Storage Bins

- Plastic Containers

- Metal Hanging Racks

- Bin Shelf & Cabinets

- Pallets

- Carts & Dollies

- More

-

CONTACT

-

Tel:

+86 18678910217 -

E-mail:

sales03@cnpowerking.com -

Address:

No.624, Qingshan Road, Qingdao, China